Estate planning has a mythology problem. Most of what people "know" about wills, probate, and inheritance comes from cocktail party conversations, television, or a vague memory of what happened when a grandparent died. The result is a set of widely believed myths that lead to expensive mistakes -- mistakes that only become visible when it's too late to fix them.

Here are the five most costly misconceptions, what the law actually says, and what each one can cost your family.

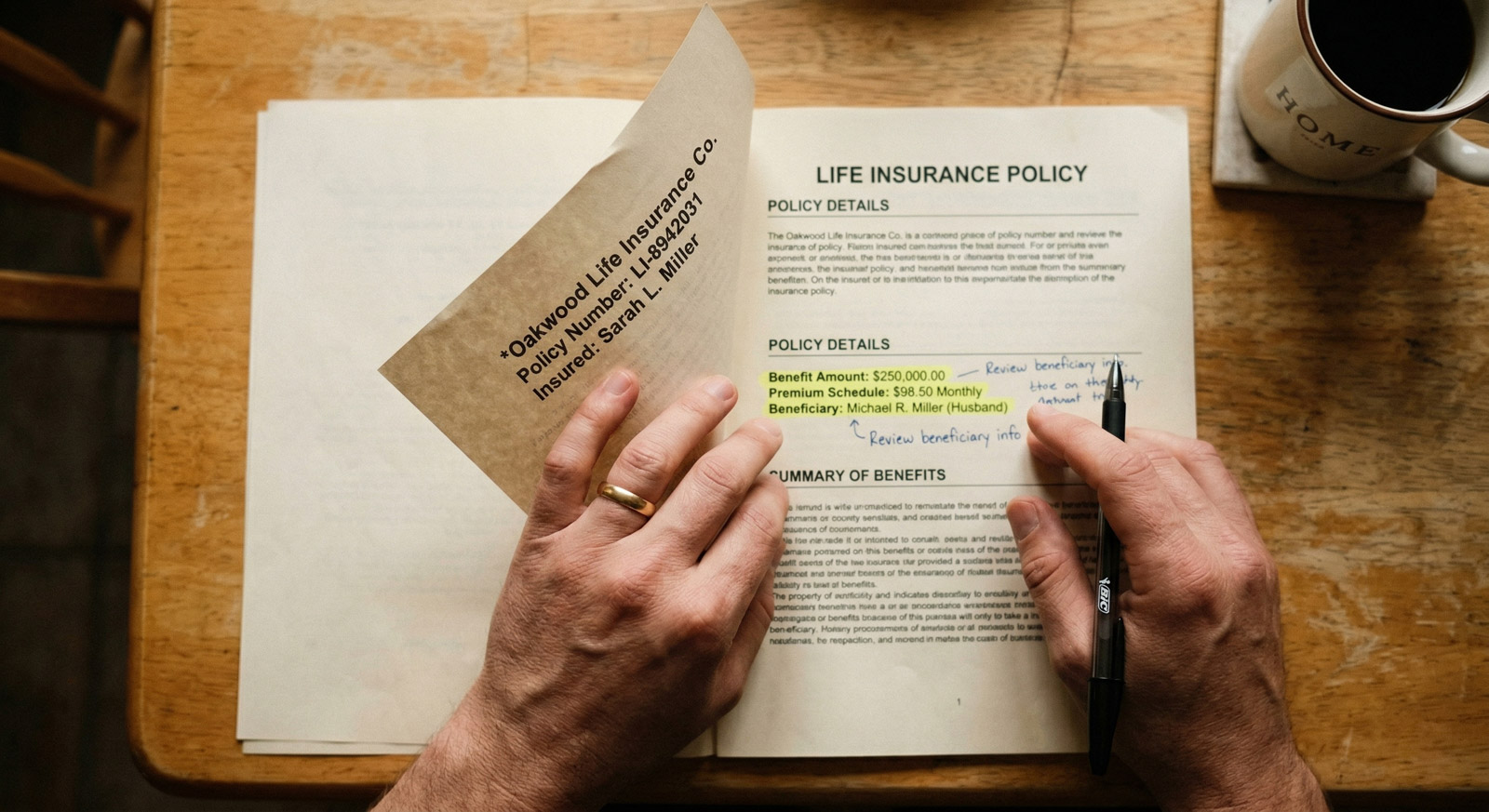

Myth 1: "My Spouse Gets Everything Automatically"

This is the most dangerous myth in estate planning, and it trips up millions of families.

If you die without a will, your state's intestacy laws decide who gets your assets. And in the majority of states, your spouse does not automatically inherit everything.[1]

Here's what actually happens in most states: if you have a surviving spouse and children, the estate is split between them. The exact formula varies by state, but common patterns include:

- Spouse gets the first $225,000 plus half the remainder (under the current Uniform Probate Code), with children splitting the rest

- Spouse gets one-third, children get two-thirds (some states)

- Spouse gets half, children split the other half (many states)

In community property states like California and Texas, the rules are different -- community property (assets acquired during the marriage) typically passes to the surviving spouse, but separate property (assets from before the marriage or received as gifts/inheritance) may be split with children.[2]

The practical impact: imagine a family with a home, some savings, and retirement accounts. The surviving spouse may need to negotiate with their own children -- or a court-appointed guardian for minor children -- to keep the family home. In blended families, this gets even more complicated, because the spouse is splitting the estate with step-children from a prior marriage.

What it costs: Legal fees to petition the court for a larger share, potential forced sale of the family home, family conflict. A will that says "everything to my spouse" would have cost a fraction of what the intestacy process costs.

Myth 2: "I'm Too Young to Need a Will"

This one sounds reasonable on the surface. If you're 30 and healthy, estate planning feels like something you can defer to your 50s. But the math doesn't support waiting.

A will isn't primarily about dying. It's about dying unprepared. And the people most affected by the absence of a will are often young families with minor children.

Without a will:

- No one is named as guardian for your children. If both parents die, the court decides who raises your kids. The judge will try to choose a suitable relative, but they're working blind -- they don't know your family dynamics, your preferences, or which relatives you'd trust with your children.[3]

- Your assets pass by intestacy. As we covered above, that means a state formula decides the split -- not you.

- Your partner may have no access to your accounts. If you're not married, your partner inherits nothing under intestacy in any state. Even married partners can face weeks or months of frozen accounts while the court process plays out.

The irony: young families often have the most to lose from not having a will, because they're the ones with minor children who need guardians named. A 65-year-old with adult children has fewer urgently dependent people.

What it costs: Court-appointed guardianship proceedings ($5,000-$15,000+), potential for children placed with a relative you wouldn't have chosen, assets stuck in limbo during the most financially vulnerable period for a surviving spouse.

Myth 3: "A Will Avoids Probate"

This is one of the most common misconceptions in estate planning, and the confusion is understandable. If you have a will, why would a court need to get involved?

The answer: a will doesn't avoid probate -- a will goes through probate. That's literally what probate is. The court reads your will, confirms it's valid, supervises the payment of debts, and authorizes the executor to distribute assets. The will is the instruction set; probate is the process of carrying out those instructions under court oversight.[4]

What does avoid probate:

- Beneficiary designations on retirement accounts, life insurance, and POD/TOD accounts

- Joint tenancy with right of survivorship (assets pass automatically to the surviving owner)

- Revocable living trusts (assets held in trust are distributed by the trustee, not by a court)

- Transfer-on-death deeds (available in about 30 states for real estate)

A will is still essential -- it handles everything that doesn't have a beneficiary designation, names your executor, and names guardians for your children. But if your primary goal is to keep assets out of court, you need a different set of tools.

For a deeper comparison of when a will is sufficient versus when you need a trust, see Will vs. Trust: Which One Do You Actually Need?. And for a plain-English walkthrough of the probate process, see What Is Probate?.

What it costs: The cost of the misconception is usually the cost of probate itself. Families who thought a will would keep them out of court are surprised to find themselves in a 6-18 month process costing 3–7% of the gross estate. In high-cost probate states, that's thousands of dollars that better planning could have avoided.

Myth 4: "Joint Accounts Solve Everything"

This myth usually sounds like: "Just put my kid's name on the bank account -- that way they get it when I die without any legal hassle."

It's technically true that jointly held accounts with right of survivorship pass automatically to the surviving owner. But using joint accounts as an estate planning strategy creates problems that are far worse than the probate costs you're trying to avoid.

Creditor exposure

The moment you add someone as a joint owner on your bank account, that money is legally accessible to their creditors. If your adult child gets sued, goes through a divorce, or has a judgment entered against them, your savings can be seized to satisfy their debts.[5]

Gift tax implications

Adding a non-spouse to a bank account or real estate deed may trigger gift tax reporting requirements. If the account balance exceeds the annual gift tax exclusion ($19,000 in 2026), you may need to file a gift tax return.

Loss of control

A joint owner can withdraw funds at any time -- legally. You've given them equal access to the entire account. If the relationship sours or if they have financial problems, there's no legal mechanism to stop them from emptying the account.

Unequal distribution

If you have three children but only add one as a joint owner on your accounts, that child receives everything in those accounts by operation of law -- regardless of what your will says. Joint ownership overrides your will. The other two children get nothing from those accounts, even if you intended an equal split.

The better alternative

Payable-on-death (POD) designations accomplish the same goal -- your bank account passes directly to a named person without probate -- but without any of the joint-ownership risks. The named beneficiary has no access to the account while you're alive, no creditor exposure, and no control over your money. Every major bank offers this option.

What it costs: Creditor seizure of joint accounts, unintended disinheritance of other children, family lawsuits over unequal distributions. These consequences routinely cost families tens of thousands of dollars -- far more than the probate costs the joint account was supposed to avoid.

Myth 5: "I Can Just Tell People What I Want"

Verbal promises about inheritance feel natural. You tell your daughter she'll get the house, your son he'll get the retirement accounts, your best friend they'll be guardian of the kids. Everyone knows what you wanted. Problem solved.

Except verbal wishes have zero legal force in estate law.

When you die, the only things that matter are:

- Written documents -- your will, trust, and beneficiary designations

- State law -- intestacy rules, if you have no written documents

Everything else -- conversations, promises, handshake agreements, emails, even text messages -- is legally irrelevant in most jurisdictions. A few states allow certain types of informal wills (called "holographic" wills) if they're written entirely in your own handwriting and signed, but even those face frequent legal challenges.[6]

The problems with relying on verbal wishes:

- Memory is unreliable. You told your daughter one thing five years ago. Your son remembers a different conversation. Neither is lying -- they just remember differently.

- People disagree. Even when everyone knows what you intended, disagreements about "what they really meant" are the fuel for estate litigation. Written documents remove ambiguity.

- Courts can't enforce what isn't written down. A probate judge distributes assets based on documents and law. They can't ask the deceased person what they wanted.

- Verbal promises create resentment. When one child was "promised" the lake house but the will says something different (or there is no will), the result is a family conflict that can last years.

“"The biggest estate planning mistakes don't come from bad documents -- they come from no documents at all." -- American College of Trust and Estate Counsel[7]”

What it costs: Estate litigation over contested verbal promises averages $10,000-$50,000+ per party. Beyond the money, the family relationships destroyed by inheritance disputes rarely recover.

The Common Thread

All five myths share the same root cause: assuming that common sense matches the law. It makes intuitive sense that your spouse would get everything. It feels reasonable that a will keeps you out of court. It seems easier to just add a kid to the bank account.

But estate law doesn't follow common sense -- it follows statutes. And statutes were written to handle the broadest possible range of situations, not your specific family. That's why a plan that reflects your specific wishes matters so much.

The good news: none of these myths are hard to overcome. A basic will addresses myths 1, 2, and 5. Understanding the distinction between wills and probate-avoidance tools (myth 3) takes five minutes of reading. And replacing joint-account strategies with proper beneficiary designations (myth 4) is free -- you can do it online in a single afternoon.

What You Can Do This Week

Check your state's intestacy laws. Find out what actually happens to your assets if you die without a will. The answer will motivate you faster than any article can.

Name a guardian in a will. If you have minor children, this is the single most important thing you can do. Heirloom can help you draft the key provisions.

Review your account ownership. If you've added adult children to bank accounts or real estate deeds as a shortcut, consider switching to POD/TOD designations instead. Same result, none of the risk.

Put your wishes in writing. Whatever you've been meaning to tell your family about who gets what -- write it down in a legal document. Conversations are important, but they don't hold up in court.

Update your beneficiary designations. These designations override your will, so they need to reflect your current wishes, not the wishes you had when you opened the account.

Sources:

- Nolo, Intestate Succession: What Happens If You Die Without a Will

- Internal Revenue Service, Community Property (Publication 555)

- American Bar Association, Guardianship and Conservatorship

- Cornell Law Institute, Probate

- FDIC, Joint Ownership of Deposit Accounts

- Uniform Law Commission, Uniform Probate Code

- American College of Trust and Estate Counsel, Estate Planning Essentials