If you died tomorrow, do you know who gets your house? Your retirement savings? Your children?

Most people don't. And the numbers are staggering: Caring.com's 2024 Wills and Estate Planning Study found that only 32% of Americans currently have a will — a six-point drop from the prior year and the first decline since 2020.[1] That means roughly two out of three adults have no say in what happens to their money, their property, or their kids when they die.

The uncomfortable truth is that if you don't write a will, your state already has one written for you. It's called intestacy law, and it's a rigid, one-size-fits-all formula that treats every family the same. It doesn't know your family. It doesn't care about your wishes. And it almost certainly won't do what you'd want.

Your State Has a Default Plan (and You Won't Like It)

When someone dies without a will, they die "intestate." That doesn't mean their assets go to the government — that's a common myth. Instead, the state distributes everything according to a fixed statutory formula based entirely on bloodlines and marriage certificates.

These formulas vary by state, but they all share the same logic: spouse first, then children, then parents, then siblings, then increasingly distant relatives. The formula doesn't account for relationships, needs, or your actual intentions.

Let's make this concrete. In New York, under Estates, Powers and Trusts Law § 4-1.1, here's what happens if you die with a spouse and children:[2]

- Your spouse gets the first $50,000 plus one-half of the remaining estate.

- Your children split the other half equally.

So if your estate is worth $500,000, your spouse receives $275,000 and your children divide $225,000. That might sound reasonable until you realize your spouse now has to fund the mortgage, raise the kids, and maintain the household on just over half of what you built together.

Under the Uniform Probate Code — adopted in some form by roughly 18 states — the surviving spouse's share depends on whether the deceased had children from a prior relationship.[3] If all children are shared, the spouse typically inherits everything. But if there are children from a previous marriage, the spouse may receive the first $225,000 plus half the balance (UPC § 2-102), with the rest going to descendants. These are UPC model amounts — your state's figures may differ.

**Try it yourself:** [See exactly how your state would distribute your estate →](/tools/intestacy-calculator)

The Spouse Surprise

Most married people assume their spouse inherits everything. It feels obvious. You're a team. You built everything together. Of course it all goes to them.

Except in most states, it doesn't.

The New York example above is not unusual. In many states, a surviving spouse receives somewhere between one-third and one-half of the estate when children are in the picture — even when those children are minors who live in the same house. Your ten-year-old doesn't need a share of the estate right now. Your spouse does. But intestacy law doesn't make that distinction.

Worse, when minor children inherit, their share typically goes into a court-supervised custodial account. Your spouse may need to petition the court just to access funds that are earmarked for the kids — funds that might be needed to pay for the kids' school, clothes, or medical bills. It creates a paperwork nightmare at the worst possible time.

“Intestacy law doesn't ask who needs the money. It follows a formula. And formulas don't raise families.”

Who Gets Nothing

Here's who intestacy law completely ignores:

- Unmarried partners. You've been together for 15 years, share a home, and raise children together — but if you're not legally married, your partner gets nothing. Not a dollar, not a dish.

- Stepchildren. You raised them since they were four. You helped with homework, drove them to practice, paid for their braces. In the eyes of intestacy law, they don't exist unless you legally adopted them.

- Close friends. Your best friend who would take a bullet for your family? Zero.

- Godchildren. The child you promised to look after? The law doesn't recognize promises.

- Charities. The organizations that matter most to you receive nothing under intestacy.

The only way any of these people receive anything is if you put it in writing. A will is the only document that lets you direct assets beyond the bloodline formula.

The Guardian Problem

This is the one that should keep every parent up at night.

If both parents die without naming a guardian in a will, a court decides who raises your children. A judge — someone who has never met your family, doesn't know your values, and has a packed docket — will make the single most important decision about your children's lives.

The court will try to place kids with a relative, but "trying" involves petitions, hearings, home studies, and months of legal proceedings. In the interim, your children may be placed in temporary foster care. Relatives you'd never choose might petition for custody. Family members may disagree, turning your children's future into a courtroom fight.

Naming a guardian in your will doesn't guarantee the court will follow your choice, but it carries enormous weight. Judges almost always defer to a parent's written wishes. Without that document, you've handed the decision to a stranger in a robe.

The Beneficiary Trap

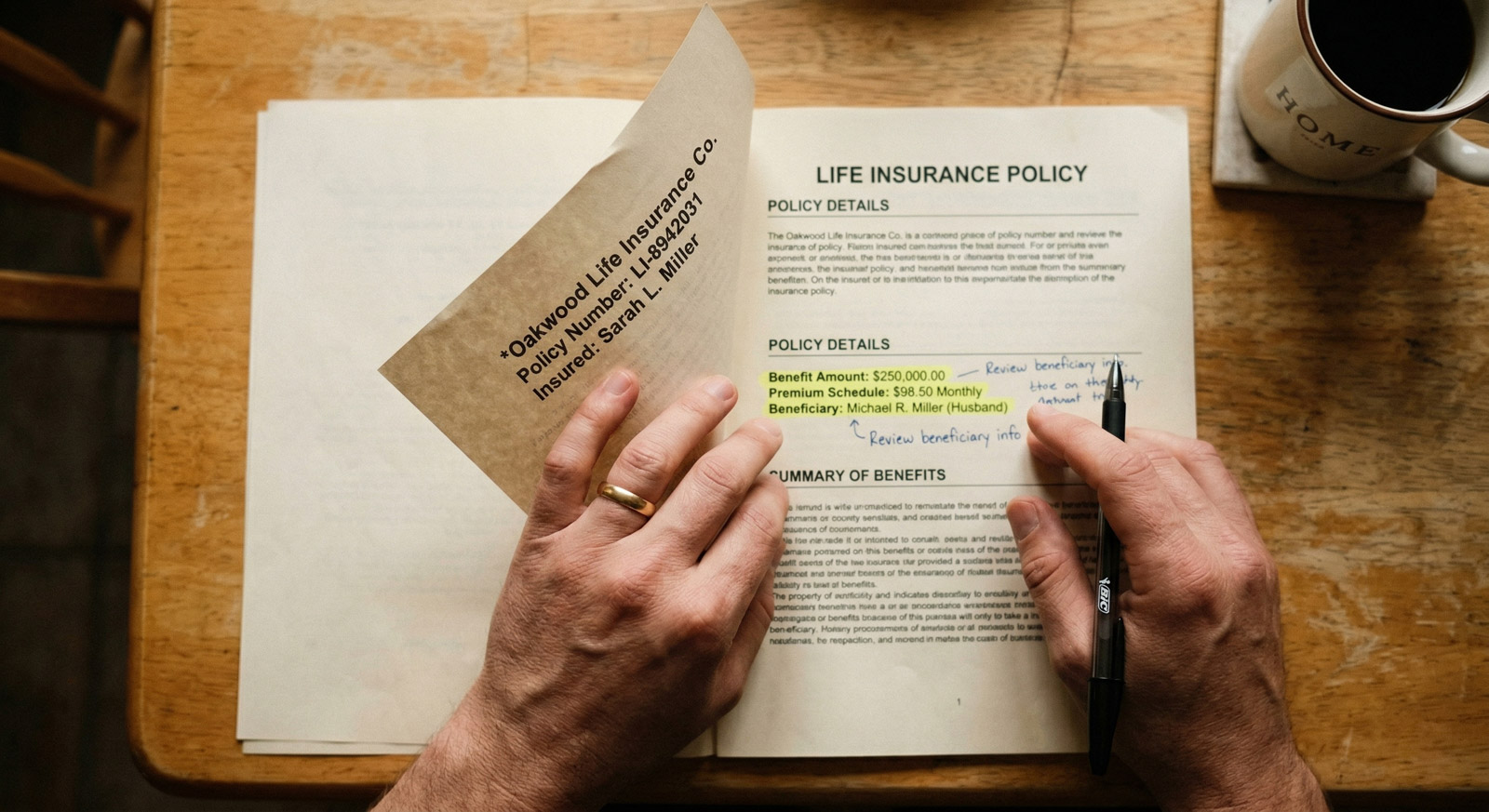

Here's a twist that catches even people who do have a will: certain assets bypass your will entirely. Retirement accounts, life insurance policies, and payable-on-death bank accounts are all controlled by beneficiary designations — the forms you filled out when you opened the account.[4]

That means the beneficiary form you filled out at your first job in 2012 might still list your ex-spouse. Your will can say "everything goes to my current wife." It doesn't matter. The beneficiary designation wins. Every time.

This isn't a hypothetical. Courts have repeatedly ruled that beneficiary designations override wills. The financial institution holding your 401(k) is legally required to pay whoever is named on that form, regardless of what your will says, regardless of your divorce decree, and regardless of what everyone agrees you "would have wanted."

The fix is deceptively simple: review your beneficiary designations every year. Check your 401(k), your IRA, every life insurance policy, and every bank account with a transfer-on-death designation. Make sure the names match your current wishes.

“Your will controls what goes through probate. But your retirement accounts, life insurance, and POD designations answer to a different document entirely — and most people haven't looked at theirs in years.”

The Four Documents Everyone Needs

A will is essential, but it's not the only document that matters. There are four legal documents every adult should have in place, regardless of age, wealth, or family situation.

1. Last Will and Testament Directs where your assets go, names guardians for minor children, and appoints an executor to manage the process. Without one, the state decides everything.

2. Healthcare Proxy (Medical Power of Attorney) Names someone to make medical decisions if you can't speak for yourself. Without one, your family may need a court order to authorize treatment — even in an emergency.

3. Financial Power of Attorney Gives someone you trust the legal authority to manage your finances — pay bills, access accounts, handle insurance claims — if you're incapacitated. Without one, your bills don't stop just because you're in the hospital.

4. Living Will (Advance Directive) Spells out your wishes for end-of-life care. Do you want to be kept on life support? Under what conditions? A living will removes the guesswork and the guilt from your family's shoulders.

Probate: The Cost of Inaction

Even with a will, your estate likely goes through probate — the court-supervised process of validating your will, paying debts, and distributing assets. But dying without a will makes probate slower, more expensive, and far more invasive.

Here's what probate typically costs:

- Time: Most estates take 6 to 18 months to settle through probate, with contested or complex estates stretching well beyond two years.[5]

- Money: Probate costs commonly run 3% to 7% of the estate's total value, including court fees, executor fees, attorney fees, and appraisal costs.[6] On a $500,000 estate, that's $15,000 to $35,000 that could have gone to your family. For a full breakdown of what probate involves, see What Is Probate?.

- Privacy: Everything filed in probate becomes public record. Your assets, your debts, who inherited what — anyone can look it up. For families that value privacy, this is a significant cost that never shows up on a bill.

Dying intestate makes all of this worse. Without a named executor, the court appoints an administrator. Without clear instructions, disputes are more likely. Without a plan, everything takes longer.

What You Can Do This Week

You don't need to overhaul your entire financial life this week. But you can take five concrete steps that will put you ahead of two-thirds of the country.

1. Check your beneficiary designations — today. Log into your 401(k), IRA, and life insurance accounts. Look at who is listed. If the names don't match your current wishes, update them. This takes 15 minutes and costs nothing.

2. Have the guardian conversation tonight. If you have minor children, sit down with your spouse and answer one question: if something happened to both of you, who should raise your kids? Write the name down. You can formalize it later, but having the conversation is the critical first step.

3. Make a list of your four documents. Do you have a will? A healthcare proxy? A financial power of attorney? A living will? Write down which ones you have and which ones you're missing. Knowing the gap is half the work.

4. Start your will this weekend. You don't need to pay a lawyer thousands of dollars to get a basic will in place. Heirloom's guided will tool helps you create a legally sound document in under an hour. A simple will now beats a perfect will "someday." Not sure whether you need just a will or also a trust? See Will vs. Trust: Which One Do You Actually Need?.

5. Set a calendar reminder to review everything in six months. Estate planning isn't a one-time event. Marriages, births, divorces, new jobs, new assets — any of these can make your existing documents outdated. Put a recurring reminder on your calendar to review your will and beneficiary designations twice a year.

The state has a plan for your family. It just isn't a very good one. The only way to overrule it is to write your own.