When someone dies, their assets don't just transfer automatically. In most cases, a court has to verify who gets what. That process is called probate -- and it's the single most common reason people feel urgency about estate planning.

The word sounds intimidating, but the concept is straightforward: probate is the legal process where a court validates a deceased person's will (if one exists), ensures debts and taxes are paid, and then authorizes the distribution of remaining assets to the right people.

If you've ever heard someone say "we're stuck in probate" or "the house is tied up in court," this is what they're talking about. Let's walk through how it actually works.

How the Probate Process Works

Probate follows a predictable sequence of steps in every state, even though the details vary. Here's the general flow:

Step 1: Filing the petition

Someone -- usually the person named as executor in the will -- files a petition with the local probate court. If there's no will, a family member files to be appointed as administrator. The court then formally opens the probate case.[1]

Step 2: Notifying interested parties

The court requires that beneficiaries, heirs, and creditors be notified. In most states, this includes publishing a notice in a local newspaper. Creditors typically have a window -- often 3 to 6 months -- to file claims against the estate.

Step 3: Inventorying assets

The executor compiles a complete inventory of the deceased person's assets: real estate, bank accounts, investments, vehicles, personal property. This inventory is filed with the court and becomes part of the public record.

Step 4: Paying debts and taxes

Before anything goes to beneficiaries, the estate's debts must be paid. This includes outstanding bills, final income taxes, and any estate taxes owed. The executor is responsible for ensuring all legitimate claims are settled.

Step 5: Distributing assets

Once debts are paid and the waiting period for creditor claims has passed, the court authorizes the executor to distribute remaining assets according to the will. If there's no will, assets are distributed according to the state's intestacy laws -- which may not match what the deceased person would have wanted.[2]

Step 6: Closing the estate

The executor files a final accounting with the court, showing every dollar that came in and went out. Once the court approves, the estate is officially closed and the executor is released from their duties.

How Long Does Probate Take?

The honest answer: longer than most people expect.

A straightforward estate with no disputes typically takes 6 to 12 months from filing to final distribution. But "straightforward" is doing a lot of work in that sentence. The American Bar Association estimates that probate takes an average of about 16 months nationally.[1]

Factors that extend the timeline:

- Contested wills. If someone challenges the validity of the will or disputes their share, litigation can add months or years to the process.

- Complex assets. Business interests, real estate in multiple states, or assets that are difficult to value (art, collectibles, intellectual property) require appraisals and additional court oversight.

- Creditor disputes. If creditors file claims that the executor contests, the court has to resolve those disagreements.

- Court backlogs. Some jurisdictions simply move slower than others. Urban probate courts with heavy caseloads can create delays that have nothing to do with the complexity of your estate.

- Missing documents. If the will can't be located, if beneficiaries can't be found, or if the deceased person's financial records are disorganized, every step takes longer.

In the best case, a simple estate in a state with streamlined probate procedures might close in 4 to 6 months. In contested or complex cases -- especially in states like California or New York -- probate can stretch to 2 years or more.

What Does Probate Cost?

Probate isn't free. The estate pays for court filing fees, attorney fees, executor compensation, and sometimes appraiser and accountant fees. All told, probate typically costs between 3% and 7% of the estate's gross value (higher in expensive states like California or New York) -- though the range is wide depending on your state.[1]

Here's what drives the cost:

Attorney fees

This is usually the largest expense. In some states (notably California), attorney fees are set by statute based on the gross estate value. On a $500,000 estate in California, the statutory attorney fee is $13,000.[3] In other states, attorneys charge hourly or negotiate a flat fee, which can range from $3,000 to $10,000 or more depending on complexity.

Executor compensation

Executors are entitled to payment for their work, though many family-member executors waive the fee. When claimed, executor fees are typically a percentage of the estate (1-5%), often mirroring the attorney fee schedule.

Court and filing fees

These vary by jurisdiction but are generally modest -- a few hundred to a couple thousand dollars.

Appraiser fees

If real estate, business interests, or other hard-to-value assets are involved, professional appraisals may be required. These can range from $300 to $5,000 per asset.

A rough state-by-state comparison

- Expensive: California, New York, Florida -- statutory fee schedules or complex processes; 4-8% of gross estate

- Moderate: Pennsylvania, Illinois, New Jersey -- typical attorney-driven costs; 3-5%

- Affordable: Texas, Wisconsin, Arizona -- independent administration or streamlined procedures; 1-3%

Your state's probate cost is one of the most important factors in deciding whether a trust is worth the investment.

What Goes Through Probate (and What Doesn't)

Here's the part that surprises most people: a significant portion of your assets may skip probate entirely, regardless of whether you have a will or a trust.

Assets that typically go through probate

- Real estate titled solely in your name

- Bank accounts in your name only (without a payable-on-death designation)

- Vehicles titled in your name

- Personal property (furniture, jewelry, art)

- Business interests

- Investment accounts without a transfer-on-death designation

Assets that bypass probate

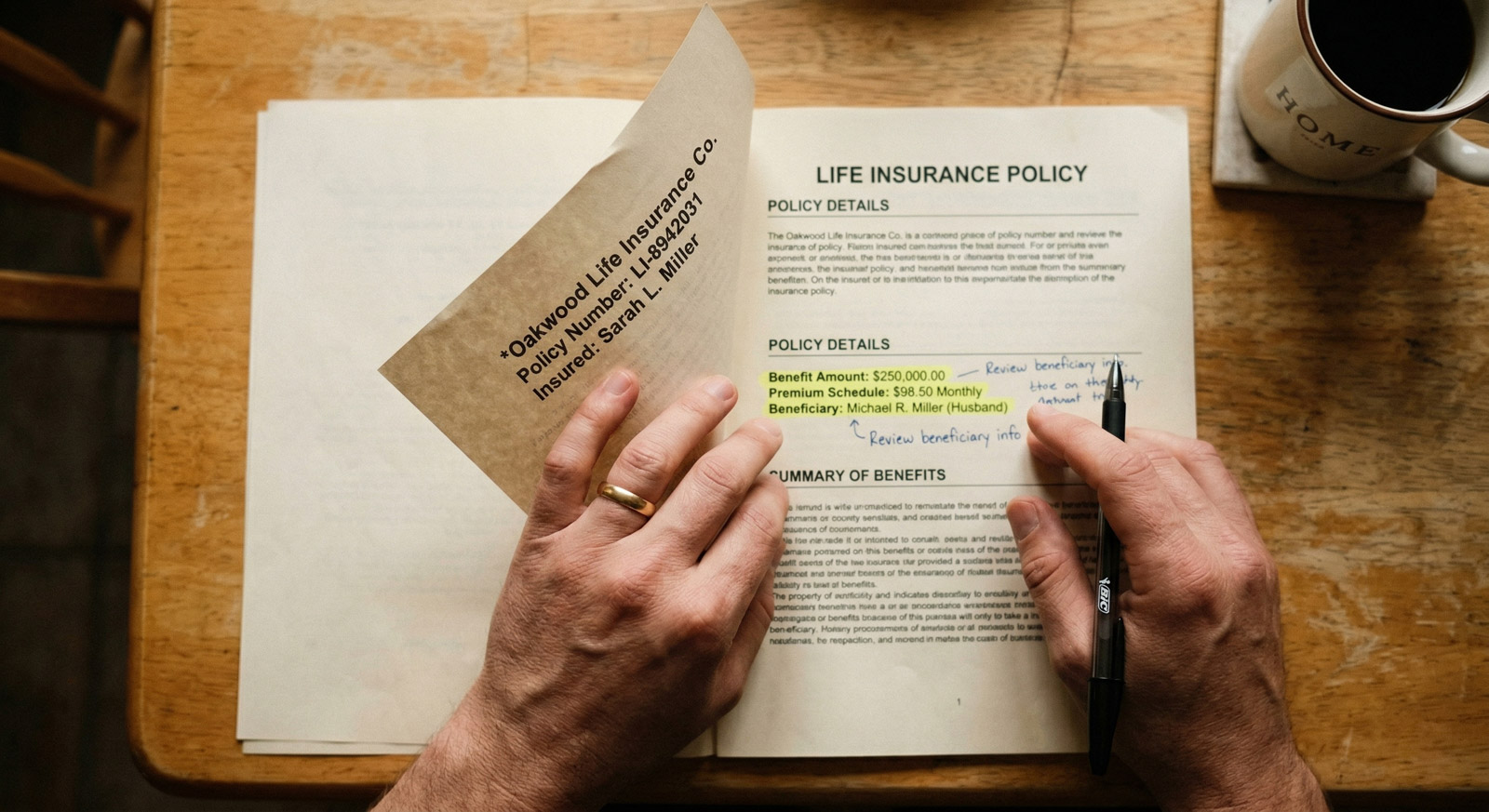

- Retirement accounts (401k, IRA, 403b) -- pass directly to named beneficiaries

- Life insurance -- paid to named beneficiaries

- Joint tenancy with right of survivorship -- passes automatically to the surviving owner

- Payable-on-death (POD) bank accounts -- transfer directly to the named person

- Transfer-on-death (TOD) brokerage accounts -- same concept for investment accounts

- Assets held in a trust -- distributed according to trust terms, no court involved

This is why beneficiary designations are so important. For many families, the majority of their wealth -- retirement accounts, life insurance, jointly held property -- already bypasses probate. The assets that actually go through probate may be smaller than you think.

How to Simplify or Avoid Probate

If you live in a state where probate is expensive or slow, there are legitimate ways to reduce the burden:

1. Keep beneficiary designations current

This is the single most effective and cheapest probate avoidance strategy. Retirement accounts, life insurance, and bank accounts with POD designations all skip probate. Make sure every account that offers a beneficiary designation has one -- and that it names the right person. An outdated beneficiary designation can override everything else in your estate plan.

2. Use transfer-on-death deeds (where available)

About 30 states now allow TOD deeds for real estate. These let you name a beneficiary for your home without creating a trust. The beneficiary gets the property when you die, without probate. You retain full control while you're alive -- you can sell the property, refinance it, or change the beneficiary anytime.

3. Hold property in joint tenancy

Assets held in joint tenancy with right of survivorship pass automatically to the surviving owner. This is common for married couples holding a home together. But be cautious about adding children as joint tenants -- it can create gift tax issues and expose the property to their creditors.

4. Set up a revocable living trust

A trust is the most comprehensive probate avoidance tool, but it's also the most expensive to set up and maintain. Assets transferred into the trust skip probate entirely. This makes the most sense for large estates, multi-state property owners, and people in high-cost probate states.

5. Check if your state has a small-estate exception

Many states allow estates below a certain threshold to skip formal probate through a simplified affidavit process. The thresholds vary widely -- from $20,000 in some states to $150,000 or more in others. If the estate is small enough, this can save thousands in fees and months of waiting.

When Probate Actually Isn't That Bad

It's worth noting that the estate-planning industry has a financial incentive to make probate sound scarier than it is. Attorneys who specialize in trust creation benefit when you're worried about probate costs.

In reality, for many families, probate is a manageable administrative process:

- In states with independent administration (like Texas), the executor can handle most tasks without ongoing court supervision. The process is relatively fast and inexpensive.

- For estates that are mostly beneficiary-designated assets, the probate estate may be small -- just a house, a car, and some personal property. The cost of probate on that subset is much lower than the cost of setting up a trust.

- The court provides oversight. Probate has a bad reputation, but the court supervision it provides can actually protect beneficiaries. The executor has to account for every dollar. If there's a dispute, there's a judge to resolve it. That structure can be valuable when family dynamics are complicated.

The question isn't "is probate bad?" -- it's "is probate in my state, for my estate, expensive enough to justify the alternatives?" For many people, the answer is no. For others, it's a clear yes. Your state and your assets determine which camp you're in.

What Happens Without a Will (Intestacy)

If someone dies without a will, the estate still goes through probate -- but instead of following the deceased person's instructions, the court follows the state's intestacy laws. These are default rules that specify who inherits based on family relationships.

The results often surprise people:

- In most states, a surviving spouse does not automatically get everything. If there are children, the spouse typically splits the estate with them.

- Step-children inherit nothing under intestacy in every state. Only biological and legally adopted children are recognized.

- Unmarried partners inherit nothing. Regardless of how long you've been together, if you're not legally married, intestacy laws don't recognize you.

- If there are no immediate family members, assets can pass to distant relatives -- or even to the state itself.

This is why having a will matters even if your estate is simple. It ensures your assets go where you want them to go, not where a state formula sends them.

What You Can Do This Week

Look up your state's probate process. Search "[your state] probate court" and spend ten minutes understanding the general cost and timeline. This single piece of information will tell you a lot about how urgent trust planning is for you.

List your major assets and check their ownership structure. Which accounts have beneficiary designations? Which assets are jointly held? You may find that less of your estate would go through probate than you assumed.

Make sure your beneficiary designations are current. Log into your retirement accounts and insurance policies. Confirm the beneficiaries are the people you actually want to receive those assets today. If you've married, divorced, or had children since you last updated them, this is urgent.

Talk to your partner. If both of you died unexpectedly, who would handle everything? Who would raise your kids? Even a basic conversation about these questions moves you closer to a plan.

Start a will. A will doesn't prevent probate, but it makes probate dramatically simpler and ensures your wishes are followed. Heirloom can help you get the key pieces in place.

Sources:

- American Bar Association, Estate Planning Information & FAQs

- Nolo, Intestate Succession: What Happens If You Die Without a Will

- California Probate Code Section 10810, Statutory Attorney Fees

- Nolo, Which States Allow Transfer-on-Death Deeds?