There is a quiet legal principle that catches families off guard every single year: beneficiary designations override your will. It does not matter what your will says. It does not matter what you told your spouse last Thanksgiving. If the beneficiary form on your 401(k) still lists your college roommate from 2004, that is who gets the money.

This is not a rare edge case. FINRA warns that outdated or incorrect beneficiary designations are one of the most common -- and most preventable -- estate planning mistakes people make.[1] The fix takes about 30 minutes.

This guide walks you through a complete beneficiary audit: every account you need to check, what to look for, and the specific language that protects your family if something unexpected happens.

Why Beneficiary Designations Matter More Than You Think

When you die, your assets move to the next owner through one of two paths. Some assets pass through your will (or trust) and go through probate. But certain accounts -- retirement plans, life insurance policies, bank accounts with payable-on-death designations -- skip that process entirely. They transfer directly to whoever is named on the beneficiary form, regardless of what any other document says.

The IRS is explicit about this: retirement account assets pass to the designated beneficiary on file with the plan administrator, not to whomever is named in a will or trust.[2] Courts have consistently upheld this principle, even in cases where the outcome was clearly not what the account holder intended.

Think about what has changed in your life since you first opened your accounts. Marriage, divorce, new children, the death of a parent. Any of those events could mean your current designations no longer match your wishes. And if you have not looked at your beneficiary forms since you first filled them out, you are not alone -- but you are exposed to real risk.

The Accounts You Need to Audit

Here is the full list of accounts that typically carry beneficiary designations. You will want to check every one of these.

Employer-Sponsored Retirement Accounts

- 401(k) and 403(b) plans -- Contact your plan administrator or check your benefits portal. Federal law (ERISA) requires that your spouse is the default beneficiary of your 401(k) unless they sign a written waiver.[3] If you are unmarried, there is no default -- you need a designation on file.

- 457(b) plans -- Government deferred compensation plans. Same concept, but not always governed by ERISA. Check with your employer.

- Pension plans -- If you have a defined benefit pension with a survivor benefit, the beneficiary designation matters here too.

Individual Retirement Accounts

- Traditional IRA -- No spousal consent requirement (unlike a 401(k)), so the named beneficiary controls.

- Roth IRA -- Same rules as a traditional IRA for beneficiary purposes. The tax treatment is different for your heirs, but the designation mechanics are identical.

- SEP IRA and SIMPLE IRA -- If you are self-employed or own a small business, these are easy to forget.

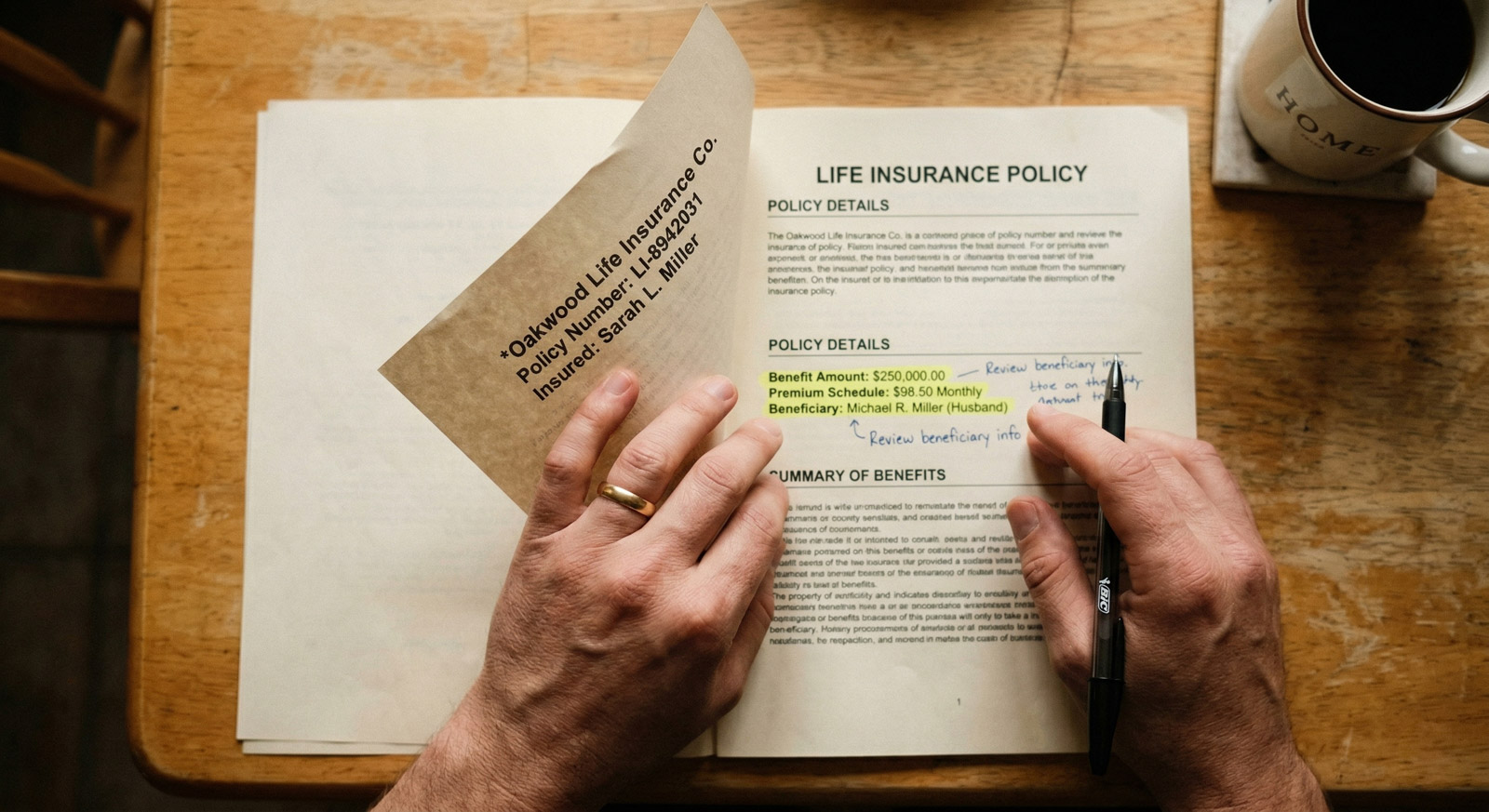

Life Insurance

- Group life insurance -- Provided through your employer. Often set up during onboarding and never revisited.

- Individual life insurance policies -- Term, whole, universal. Each policy has its own beneficiary form.

Health and Savings Accounts

- Health Savings Account (HSA) -- Many people do not realize their HSA has a beneficiary designation. If your spouse is named, they inherit it as their own HSA. Anyone else receives a taxable distribution.[4]

Bank and Brokerage Accounts

- Payable-on-death (POD) bank accounts -- Checking, savings, money market, and CD accounts can all have POD designations. The money transfers directly to the named beneficiary outside of probate.

- Transfer-on-death (TOD) brokerage accounts -- Individual and joint brokerage accounts can carry TOD registrations. The securities pass directly to the named beneficiary.

Primary vs. Contingent Beneficiaries

Every beneficiary form has (at minimum) two layers, and both matter.

Primary beneficiary -- the person (or people) who receive the account assets when you die. You can name multiple primary beneficiaries and assign percentages (for example, 50% to your spouse, 25% each to two children).

Contingent beneficiary -- the backup. If your primary beneficiary dies before you, the contingent beneficiary receives the assets. This is the safety net that most people either skip or forget to update.

Leaving the contingent beneficiary blank is a surprisingly common mistake. If your primary beneficiary predeceases you and there is no contingent named, the account typically reverts to your estate -- which means it goes through probate, may face higher taxes, and could end up distributed in ways you did not intend.

“"The biggest planning mistake we see is not the absence of a will -- it's the beneficiary form that was filled out fifteen years ago and never touched again."”

Name both. Always.

When to Use "Per Stirpes"

You will see this option on many beneficiary forms, and it solves a specific problem: what happens if one of your beneficiaries dies before you?

Per stirpes (Latin for "by the branch") means that if a beneficiary predeceases you, their share passes down to their children -- not sideways to the other beneficiaries.

Here is a concrete example. You name your three children as equal primary beneficiaries (33.3% each) with a per stirpes designation. If one of your children dies before you and has two kids of their own, those two grandchildren split their parent's one-third share. Without per stirpes, the deceased child's share would be divided between your two surviving children, and the grandchildren would receive nothing.

Nolo's estate planning resources explain that per stirpes is the most common distribution method used in estate plans because it keeps assets flowing down family lines rather than concentrating them among survivors.[5]

When per stirpes makes sense:

- You have children or grandchildren

- You want each family "branch" to receive their share, even if a member of that branch dies

- You are naming multiple beneficiaries at the same generation level

When it may not apply:

- You are naming a single beneficiary (a spouse, for instance) -- the contingent beneficiary handles the "what if" scenario instead

- You have specific wishes that differ from the default per stirpes distribution (in that case, name each person individually with explicit percentages)

The 30-Minute Audit Process

Here is the step-by-step process. Block 30 minutes, grab your laptop, and work through this list.

Step 1: Gather Your Account List (5 minutes)

Write down every account that could carry a beneficiary designation. Use the list above as your reference. Include the institution name, account type, and approximate value. If you are unsure whether an account has a designation, add it to the list -- you will check.

Step 2: Log In and Review Each Designation (15 minutes)

For each account, find the current beneficiary designation. Most institutions have this under "Account Settings" or "Beneficiaries" in their online portal. For employer plans, check your HR benefits portal.

For each account, note:

- Who is listed as primary beneficiary? Is this still correct?

- Who is listed as contingent beneficiary? Is anyone listed at all?

- Are the percentages right? If you have multiple beneficiaries, do the shares still reflect your wishes?

- Is the information current? Names, dates of birth, Social Security numbers (some forms require them), and relationships should all be accurate.

- Is per stirpes selected? If it is available and appropriate for your situation, make sure it is checked.

Step 3: Make Updates (10 minutes)

For any account that needs changes, submit the updated beneficiary form. Most institutions allow you to do this online. Some (especially employer-sponsored plans) may require a physical form or spousal consent.

If you are married and updating a 401(k) or other ERISA-governed plan, your spouse must typically sign a waiver if you want to name someone other than them as primary beneficiary. This is a federal requirement, not optional.[3]

Step 4: Document Everything

Save copies of your updated beneficiary forms. Store them alongside your will and other estate documents. If you are using a tool like Heirloom to organize your estate plan, this is a good place to note which accounts have designations and when they were last reviewed.

Common Mistakes to Watch For

The ex-spouse problem. Divorce does not automatically remove your former spouse from beneficiary designations in most states, especially for ERISA-governed retirement plans. Even if your divorce decree says otherwise, the beneficiary form controls. You must actively change it. For the full divorce-specific checklist, see Beneficiary Designations After Divorce.

The "estate" designation. Some people name "my estate" as the beneficiary on retirement accounts. This is almost always a mistake -- it forces the account through probate and can eliminate the tax-deferral benefits that an individual beneficiary would receive.[2]

Minor children as beneficiaries. If you name a minor child directly, the account may require a court-appointed guardian to manage the funds until the child reaches legal age. A trust for the child's benefit is usually a better approach. For more on how trusts and wills interact, see Will vs. Trust.

Forgetting group life insurance. Employer-provided life insurance often equals one or two times your salary. That could be $100,000 or more, controlled by a form you filled out during your first week on the job.

What You Can Do This Week

You now have the full framework. Here is the condensed checklist to get it done.

List every account with a beneficiary designation. Include 401(k), IRA, Roth IRA, life insurance (group and individual), HSA, POD bank accounts, and TOD brokerage accounts. Do not skip the small ones.

Log in to each account and review the current designations. Confirm the primary beneficiary, contingent beneficiary, percentage allocations, and per stirpes elections are all correct and current.

Update any outdated or missing designations immediately. Pay special attention to accounts that still list an ex-spouse, have no contingent beneficiary, or name "my estate."

Save copies of every updated beneficiary form. Store them with your will, trust documents, and other estate planning records so your family can find them when they need to. For the full document checklist, see The 4 Documents Every Adult Needs.

Set an annual reminder to re-audit. One review per year -- plus a check after every major life event -- keeps your designations aligned with your actual wishes.

That is the entire process. Thirty minutes now to prevent months of legal complications and potentially thousands of dollars in losses for your family later. The accounts are already open in front of you. Start with the biggest one.

Sources:

- FINRA, "Planning Ahead — Have You Chosen Your Beneficiaries?" https://www.finra.org/investors/insights/choosing-beneficiaries

- IRS, "Retirement Topics -- Beneficiary," https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-beneficiary

- U.S. Department of Labor, "FAQs About Retirement Plans and ERISA," https://www.dol.gov/agencies/ebsa/about-ebsa/our-activities/resource-center/faqs/retirement-plans-and-erisa

- IRS, "Health Savings Accounts and Other Tax-Favored Health Plans," Publication 969, https://www.irs.gov/publications/p969

- Nolo, "What Is Per Stirpes?" https://www.nolo.com/legal-encyclopedia/what-per-stirpes.html

- FINRA, "Plan Now to Smooth the Transfer of Your Brokerage Account Assets on Death," https://www.finra.org/investors/insights/plan-ahead-transfer-your-brokerage-account-assets-death